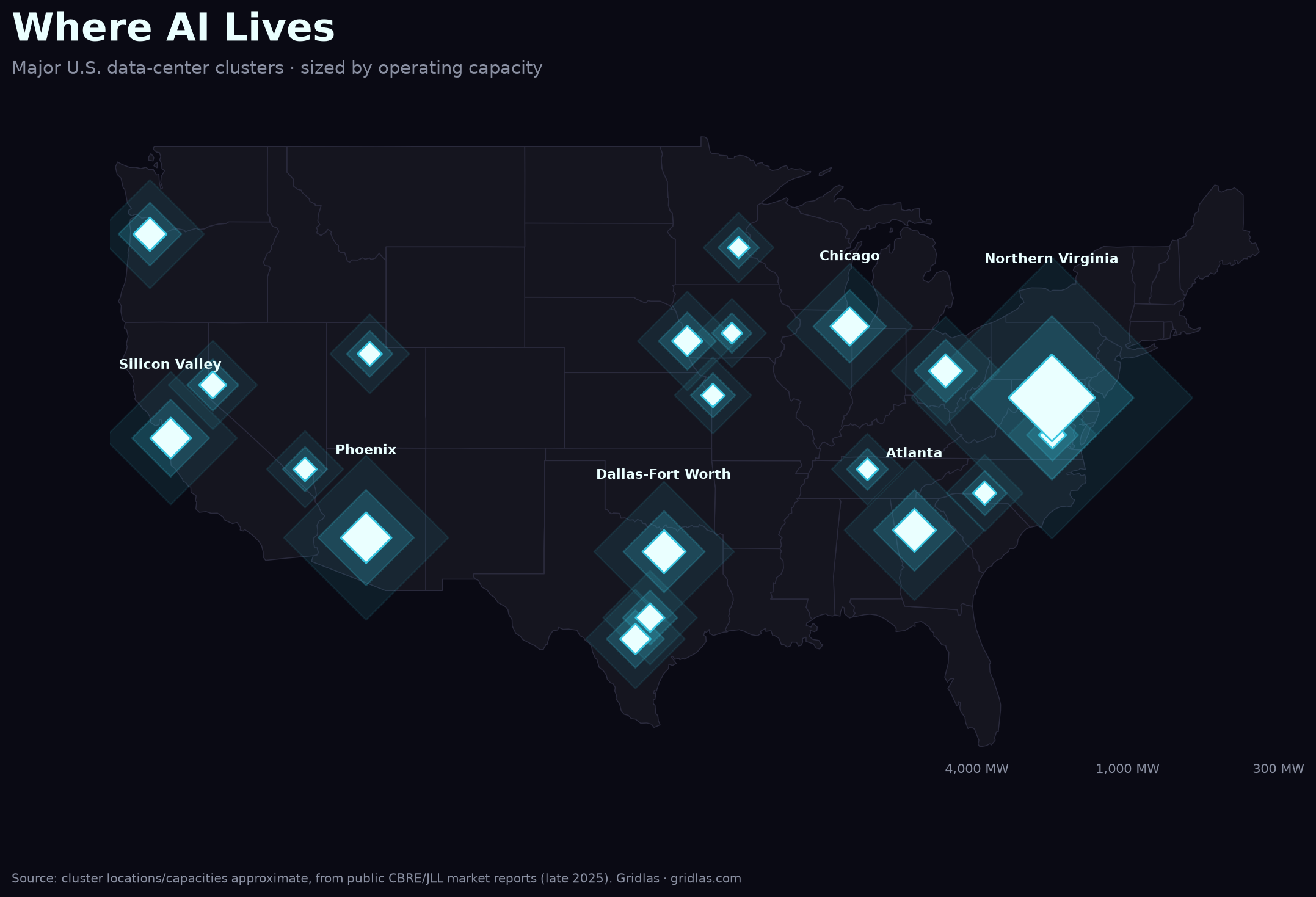

Home / Data centers by region / Nashville & Middle Tennessee

Nashville & Middle Tennessee data-center power demand

If Memphis is the operator building its own power in the open, Middle Tennessee is the utility doing it for them — TVA is rebuilding its grid around the data-center wave.

Nashville doesn't look like a hyperscale hub from the outside, but Middle Tennessee has quietly become one of the Southeast's fastest-growing data-center corridors. Cushman & Wakefield lists it among the emerging markets, and the pipeline is dense: Meta's Gallatin campus — roughly 300 MW across ~900 acres, expandable to a dozen data halls — anchors it, with Google in Clarksville, plus Flexential, Lumen, DC BLOX (~50 MW) and Fisk University's planned 30 MW "Quantum Leap" facility filling in around the metro. Notably, Meta won permission in late 2025 to expand Gallatin using tensioned-fabric "tent" structures — a tell of how fast operators want to add capacity.

The draw is TVA: historically cheap, reliable public power, and a utility that has chosen to court large loads rather than turn them away. That posture, plus the broader shift of the buildout toward the Southeast — nearly half of new U.S. data centers are headed there — has made the Tennessee Valley a magnet. Data-center electricity across the TVA region grew about sevenfold from 2020 to 2025, reaching 8.3 million MWh.

And TVA is now reorienting its entire generation plan around that demand. Data centers have gone from 1–5% of TVA's industrial load to about 18% in 2025, a share the authority expects to double by 2030, with a demand pipeline already five times its current data-center load. TVA set a new winter peak record of 35,319 MW in January 2025 and is pursuing roughly 6.2 GW of new generation — more than 3,700 MW already under construction — leaning heavily on natural gas, with incremental gas needs it pegs at 7–26 GW through 2040. It is also planning new rate structures aimed first at the AI data centers driving the load.

Why it matters

Nashville is the front-of-the-meter mirror of Memphis. Both sit in TVA territory; both answer the AI power crunch with gas. The difference is who builds it and who pays. Where Memphis put the generation — and the emissions fight — on the operator's own site, Middle Tennessee routes it through the utility, which spreads new gas plants and the cost of them across ratepayers via the same demand surge. It's the clearest case of a public utility building around the queue on the buildout's behalf.

See the full picture. The Gridlas report ranks the markets, maps them against the grid, and includes the underlying dataset (CSV/GeoJSON) — built from public EIA, LBNL & CBRE data.

Get the report →