Home / Data centers by region / Hillsboro & Oregon

Hillsboro & Oregon data-center power demand

The "Silicon Forest" is where cheap Northwest hydropower meets the Pacific's fiber. It's also nearly full — the tightest of the primary markets.

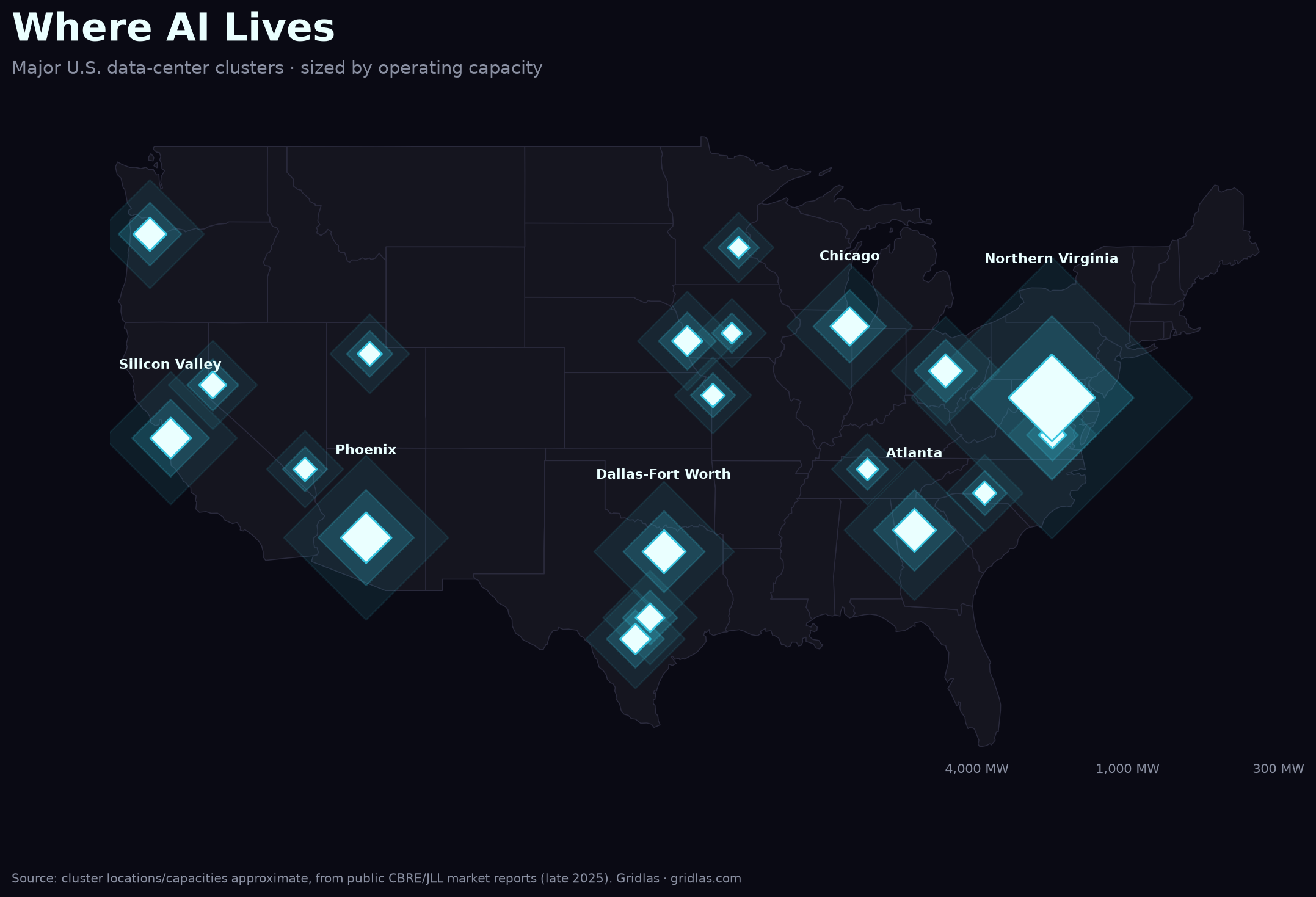

Hillsboro, on Portland's western edge, is the Pacific Northwest's data-center capital — the "Silicon Forest." Two forces built it: some of the cheapest, cleanest power in the country from the region's hydroelectric system, and Oregon's enterprise-zone property-tax abatements, which have long made large capital-intensive facilities pencil out. CBRE puts total inventory around 475 MW at the end of 2025 — enough to rank it among the eight primary U.S. markets.

What makes Hillsboro different from the inland Oregon hyperscale campuses is connectivity. It's where the Pacific's subsea cables come ashore — the U.S. landings of the New Cross Pacific and Hawaiki systems, and the Oregon landing of the U.S.–Singapore Bifrost cable — feeding the densest interconnection hub in the region. That fiber, plus hydro power, is why operators keep expanding here: NTT is bringing on an additional ~216 MW toward a planned 354 MW, and Flexential is building its fifth and planning its sixth Hillsboro facility.

But the defining number is vacancy: 0.2% at end-2025, the lowest of any primary market CBRE tracks, with roughly 1 MW of space actually available. Demand has outrun the ability to deliver powered shells. Like Silicon Valley, Hillsboro is a market where the tenants are lined up and the constraint has moved upstream — to transmission, to substations, to how fast the utility can energize the next campus.

Why it matters

Hillsboro is the Northwest's proof that clean, cheap power is necessary but not sufficient. Even with hydro and the best transpacific connectivity on the West Coast, a market fills up when new capacity can't be energized fast enough. Its 0.2% vacancy is the same story as Silicon Valley's finished-but-dark shells, told in a different grid — and another data point in why the buildout keeps fanning out to markets with spare headroom.

See the full picture. The Gridlas report ranks the primary markets, maps them against the grid, and includes the underlying dataset (CSV/GeoJSON) — built from public EIA, LBNL & CBRE data.

Get the report →