Home / Data centers by region / Reno & Northern Nevada

Reno & Northern Nevada data-center power demand

Reno sold one thing above all: speed to power. The Tahoe Reno Industrial Center is now testing whether even the fastest market can outrun its own demand.

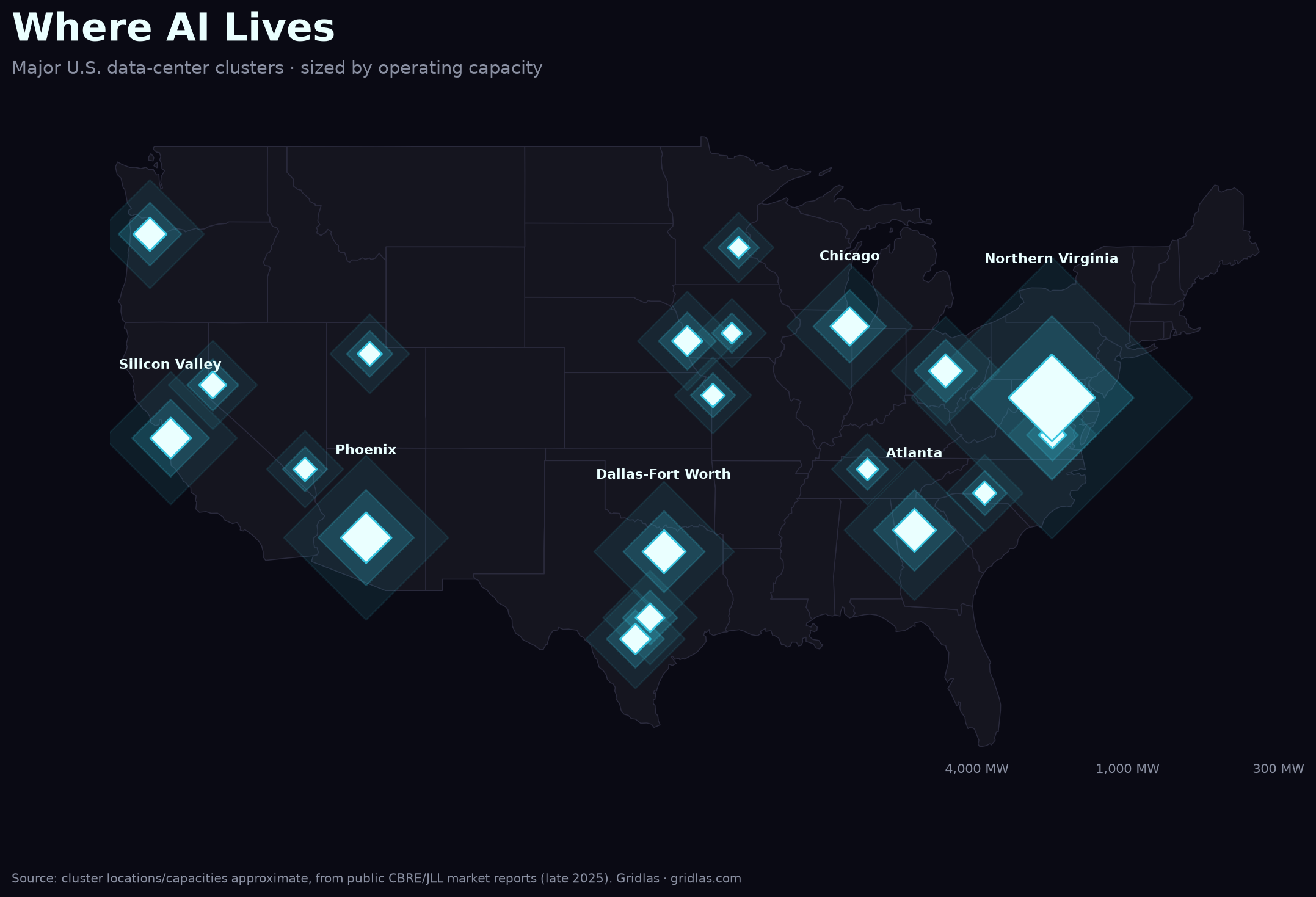

The Tahoe Reno Industrial Center (TRIC) in Storey County, just east of Reno-Sparks, is one of the West's marquee data-center addresses — home to Switch's enormous Citadel campus, with Apple, Google and Microsoft nearby. In 2025 Cushman & Wakefield ranked greater Reno-Sparks the fifth-fastest-growing emerging data-center market in the world, and newcomers keep arriving: Vantage is investing ~$3B in a 224 MW campus (NV1) whose first two buildings are already fully leased, alongside Tract, EdgeCore, Novva and others.

What Reno actually sells is a shorter path to a powered building. TRIC's Storey County permitting is famously fast, land is cheap, and the utility — NV Energy, a Berkshire Hathaway company — has openly positioned itself to deliver power to AI compute. In a buildout where the binding constraint everywhere else is time, "speed to power" is the product. That is why the capital came.

But the demand has outrun even that. NV Energy says it has received interest representing roughly 22,000 MW of potential new load — more than two and a half times the state's entire ~8,500 MW system peak — and now needs about 47% more energy than it forecast just two years ago. Data centers already draw around 22% of Nevada's electricity, a share the utility projects could reach 64% by 2046. The fast-permitting frontier has hit the same wall as everyone else: you can approve a building in months, but you can't conjure firm power or transmission on the same clock.

So the workaround is appearing here too. Fleet Data Centers has proposed building more than 350 MW of on-site natural gas and diesel generation at TRIC to power its own facilities rather than wait on the grid — the same behind-the-meter move seen in Memphis and legislated in Utah, now in the market that was supposed to be the fast one. The bridge fuel follows the compute.

Why it matters

Northern Nevada is the control case for the whole thesis. Take away slow permitting and a reluctant utility — the frictions that define Virginia or Silicon Valley — and demand still laps supply, because the real limit is firm power and wires, not paperwork. When the fastest market in the West starts self-generating with gas, it says the constraint isn't local. It's structural.

See the full picture. The Gridlas report ranks the markets, maps them against the grid, and includes the underlying dataset (CSV/GeoJSON) — built from public EIA, LBNL & CBRE data.

Get the report →