Home / Data centers by region / Salt Lake City & Utah

Salt Lake City & Utah data-center power demand

"Silicon Slopes" is the market that stopped waiting for the utility. Utah wrote the workaround into law — and the data centers are building their own power plants.

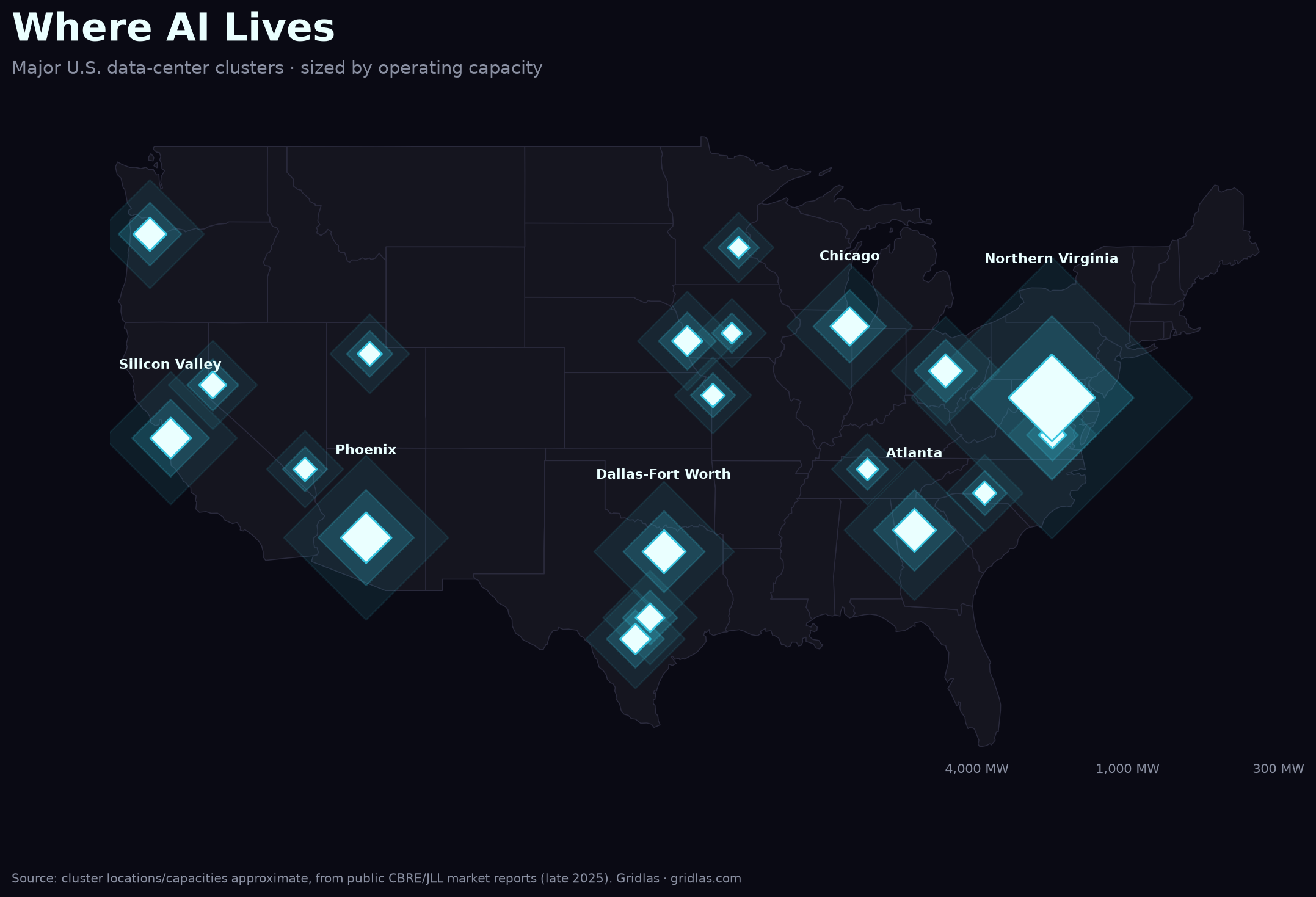

Utah's Wasatch Front — Salt Lake City, West Jordan, Bluffdale, Eagle Mountain — has quietly become one of the West's fastest-growing data-center corridors. Roughly 48 operational facilities draw about 920 MW today, with another ~2.6 GW under construction that would more than triple the state's data-center load. The draws are familiar: cheap power (retail rates near 5–6¢/kWh), aggressive tax incentives, and deep fiber. Meta anchors the market with a 504 MW campus at Eagle Mountain (a ~$7B investment); Novva, Aligned, and NSA's Bluffdale facility fill in around it.

But Utah's real significance to this project isn't its size — it's what the state did when the grid couldn't keep up. Utah's largest utility, Rocky Mountain Power (a PacifiCorp / Berkshire Hathaway Energy subsidiary), signaled it can't serve the wave of multi-hundred-megawatt requests without major new investment. So in 2025 the legislature passed SB 132: a "large load" of 100 MW or more can be pushed off the utility's duty to serve — the utility gets 90 days to evaluate, and if it can't deliver, the data center is free to build its own generation. Utah didn't just experience the interconnection bottleneck; it legislated a bypass around it.

The result is exactly the powering-around-the-queue playbook, seen at the state level. Novva Data Centers won approval in December 2024 to build a 200 MW natural-gas plant at its West Jordan campus — a data center generating its own firm power rather than waiting years in the queue. And PacifiCorp's own 2025 resource plan leans heavily on new natural gas to meet a data-center load it projects could add ~6 GW by 2030. Whether the power is built behind the meter by the operator or in front of it by the utility, the near-term answer in Utah is the same fuel.

The speculative end of the pipeline is enormous and unproven. A proposed 9 GW campus tied to investor Kevin O'Leary would, if fully built, consume more than twice all the electricity Utah uses today; the Joule campus in Delta is pitched at 1.4 GW. Treat those as ambitions, not megawatts on the grid. What's concrete is the pattern already in the ground: firm gas, self-supplied, to skip the wait — and a growing fight over the water and emissions that pattern brings to a drought-prone state.

Why it matters

Utah is the clearest policy test of the whole thesis. Everywhere else, the interconnection queue is a constraint operators endure. Utah decided the constraint was optional for anyone big enough and let them route around the utility entirely. That unblocks the buildout — and quietly shifts new firm capacity to gas, concentrates it with the largest players, and pushes the cost onto water, air, and whoever isn't a 100 MW load. It's the workaround, written into statute.

See the full picture. The Gridlas report ranks the markets, maps them against the grid, and includes the underlying dataset (CSV/GeoJSON) — built from public EIA, LBNL & CBRE data.

Get the report →