Home / Data centers by region / Iowa (Des Moines & Council Bluffs)

Iowa data-center power demand: the wind-powered cluster

The heartland became a hyperscale training hub because the wind blows cheap and constant. Now the question is whether even Iowa has enough.

Iowa is what happens when cheap, clean power meets aggressive incentives. MidAmerican Energy runs 27 wind farms across the state, and in 2024 wind supplied roughly 63% of Iowa's electricity — the highest share of any U.S. state. That combination pulled the hyperscalers in early: Microsoft's Project Alluvion in West Des Moines (six buildings, ~200 MW, $5–6B invested), Google's Council Bluffs campus ($5.5B, ~95% carbon-free), Meta's large Altoona campus, and Apple in Waukee.

The West Des Moines campus is widely reported as the home of the Microsoft supercomputer used to train OpenAI's GPT-4 — which also made Iowa an early flashpoint for the buildout's water footprint, as evaporative cooling drew on local supplies during peak training. Meta's Altoona site alone consumed about 1.2 million MWh in 2023, its second most energy-intensive data center anywhere. And with new load still arriving, Iowa is now quietly studying a nuclear revival — a tell that even a grid running majority-wind is feeling the pull of AI demand.

Why it matters

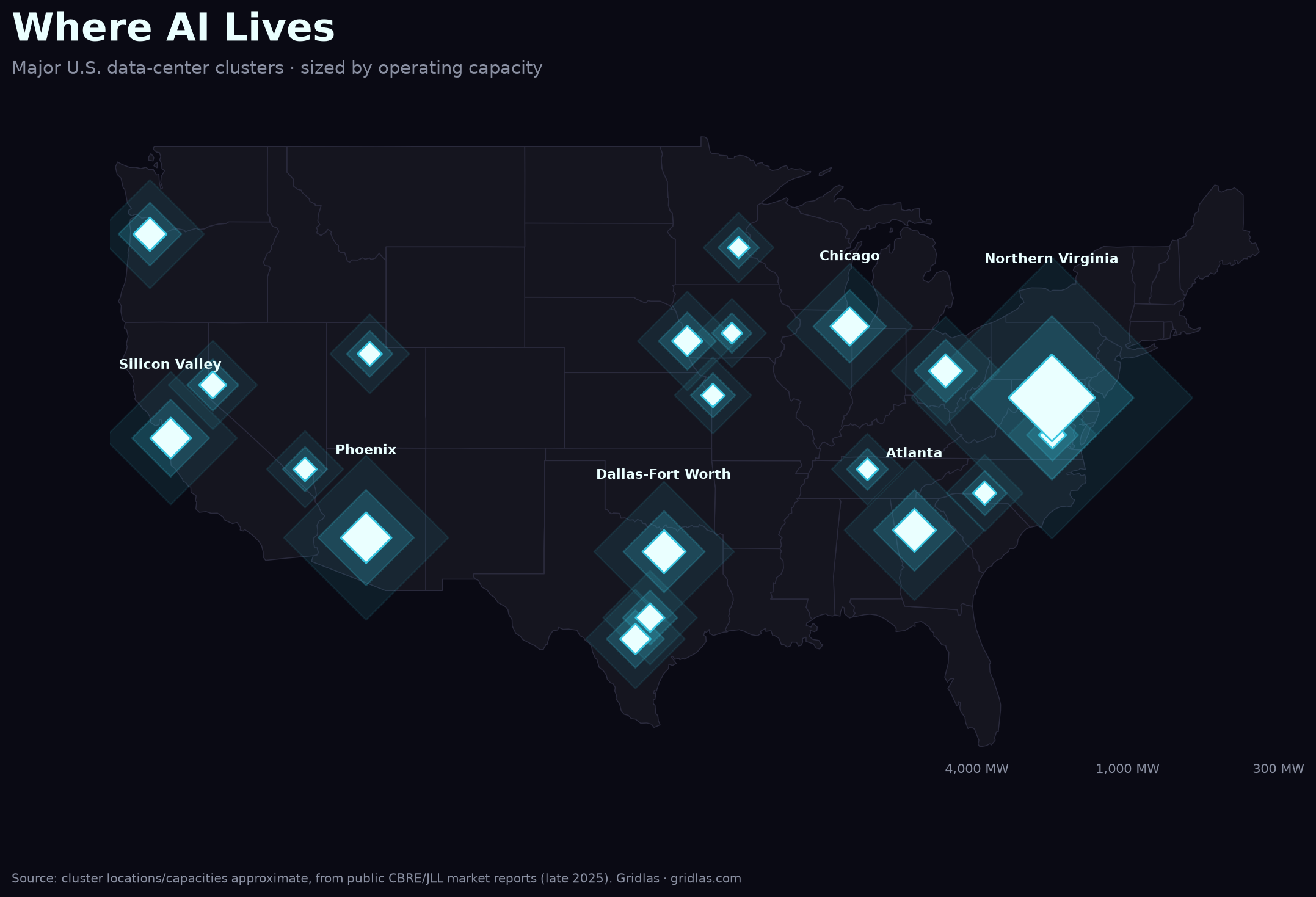

Iowa is the other end of the map from Silicon Valley and Hillsboro. Those markets prove what a ceiling looks like; Iowa shows where demand goes to find headroom — and how fast that headroom gets spent. Its wind-first grid is exactly why the compute landed here, and its emerging water, transmission, and generation questions are a preview of what "abundant" markets face next. It's a live read on the national supply-vs-demand gap the report maps.

See the full picture. The Gridlas report ranks the primary markets, maps them against the grid, and includes the underlying dataset (CSV/GeoJSON) — built from public EIA, LBNL & CBRE data.

Get the report →